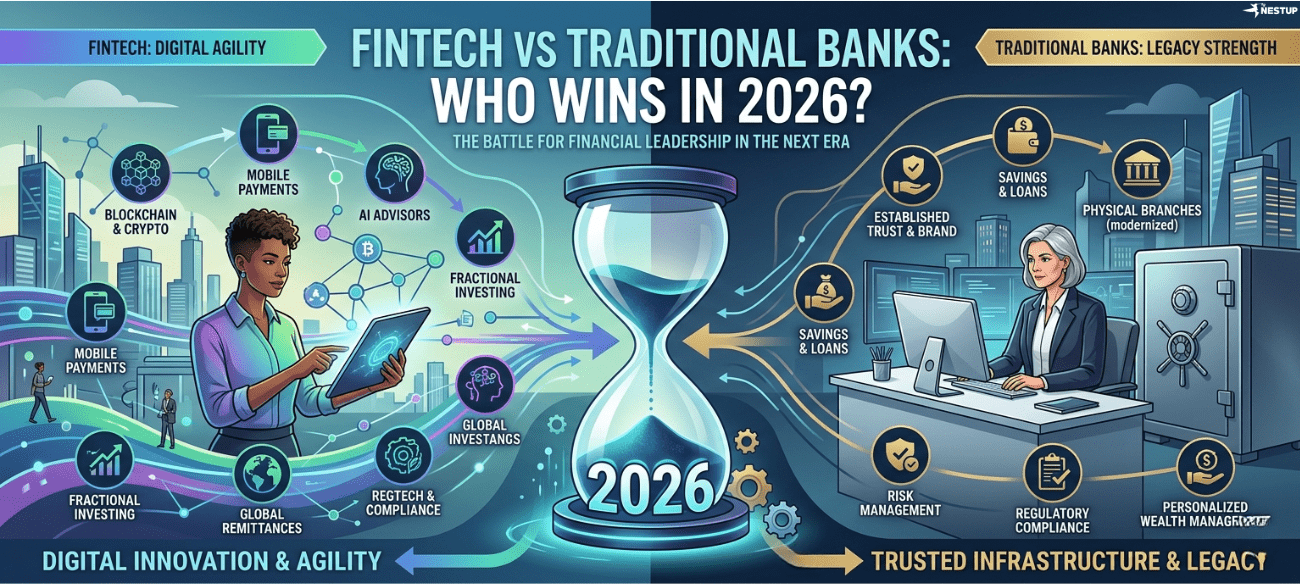

Introduction: The Great Financial Detente

In the early 2020s, the narrative was framed as an existential battle: agile fintech startups were the “bank killers,” destined to dismantle the century-old foundations of legacy institutions. Fast forward to 2026, and the battlefield has been replaced by a boardroom. The expected revolution didn’t result in the extinction of traditional giants; instead, it sparked a “Great Financial Detente.”

The battle between digital-first finance and legacy banking giants has reached a fascinating stalemate. Traditional banks didn’t disappear—they digitized. Fintechs, meanwhile, shifted from niche disruptors into comprehensive financial ecosystems. Today, the most pressing question for the digital economy isn’t which side will win, but how their convergence is fundamentally reshaping the way we move, save, and borrow money.

Takeaway 1: The “Bank Killer” Narrative Has Been Replaced by “Ecosystems”

The landscape of 2026 is defined by adaptation rather than replacement. Traditional banks survived the “insurgency” by aggressively adopting the very features that once made fintechs unique. By investing heavily in AI and automation, overhauling mobile apps, and integrating instant payment rails, legacy institutions bridged the tech gap.

At the same time, fintechs like Revolut and Chime have matured. They are no longer just “niche apps” for one-off transfers; they have evolved into serious financial ecosystems offering a broad range of services.

Analysis/Reflection: This shift represents a “survival of the fittest” through imitation. However, there is a catch. While fintechs win on speed, they often struggle with the “friction” of scale—specifically account freezes and the rigid nature of automated compliance systems. This lack of human-centric support is a key reason why the total displacement of banks never materialized; consumers still value the safety net of a legacy institution when things go wrong.

Takeaway 2: International Borders Are Where Fintechs Claimed Final Victory

While traditional banks held their ground in domestic services, fintechs won the international war by a landslide. Legacy institutions remain tethered to bureaucratic processes and a fee structure that feels increasingly archaic. While a traditional bank might still hit a customer with account maintenance fees, overdraft penalties, and opaque currency conversion spreads, fintechs have optimized for transparency.

Fintechs like Wise and Revolut were built with a “global-first” architecture. They provide transparent FX pricing and multi-currency accounts that cater specifically to the modern workforce—remote workers, freelancers, and digital nomads.

Analysis/Reflection: Cross-border finance has become the strongest category for fintech because it addressed a fundamental inefficiency. For those whose lives and businesses cross borders, the speed of digital-first platforms is irreplaceable.

“International users often save significant money with fintech platforms compared to legacy currency conversion spreads.”

Takeaway 3: The Rise of the “Hybrid Consumer” as the New Standard

By 2026, the average consumer has stopped choosing sides. The “Hybrid Consumer” is the new market standard, strategically splitting their financial life between two different types of providers to maximize utility:

- Traditional Banks: Used for high-stakes needs such as salary deposits, mortgages, business loans, and long-term savings.

- Fintechs: Used for daily spending, international travel, peer-to-peer transfers, and granular, AI-driven budgeting.

Analysis/Reflection: This “best of both worlds” approach is the most logical outcome for the modern user. It allows consumers to enjoy the cutting-edge UX of a fintech app without sacrificing the lending power and perceived “too big to fail” security of a major bank.

Takeaway 4: The Lending and Trust Barrier remains an Incumbent Fortress

Despite the rapid innovation of fintech, traditional giants like JPMorgan Chase and Bank of America still dominate the lending landscape. The reason is rooted in balance-sheet strength and regulatory trust. Traditional banks possess the massive capital required for mortgages and large-scale business underwriting, alongside a perceived stability that fintechs have yet to match.

Analysis/Reflection: There is a lingering irony here: while fintechs offer far superior software, they lack the long operating history and deep government relationships that consumers crave during times of economic stress. In a downturn, users still look to the institutions with the largest balance sheets, proving that banking is still fundamentally about the strength of the vault, not just the beauty of the interface.

Takeaway 5: Fintech Has Transformed into the “Invisible Infrastructure”

The most significant trend of 2026 is that fintech is no longer trying to replace banks; it is becoming the “invisible infrastructure” that powers them. The line is now permanently blurred. Many fintechs operate as financial interfaces (the “skin”) while legacy banks provide the necessary “plumbing”—the licenses, charters, and regulatory frameworks.

AI has become the glue of this partnership. Fintechs use AI for personalized UX and spending insights, while banks utilize it for compliance automation and risk analysis.

Analysis/Reflection: We have reached a state of convergence where banks look like apps and apps function as gateways to banking stability. The “winner” is whichever entity can integrate AI most effectively to balance personalization with security.

“The future of finance probably isn’t fintech replacing banks or banks crushing fintechs. It’s a convergence… the smartest financial systems increasingly combine fintech speed with banking stability.”

Conclusion: The Real Winner is the Consumer

The war between fintech and traditional banking may have ended in a draw, but the competition has produced a clear winner: the consumer. This decade of friction forced legacy banks to lower fees, improve their apps, and accelerate transfer speeds. Simultaneously, the regulatory requirements of banking forced fintechs to become more transparent and reliable.

As we look toward the next five years, the choice is no longer about which side will win the war. The choice is about how you manage your own portfolio. Do you value the agility of speed or the legacy of stability? Most likely, your wallet in 2031 will depend on a sophisticated mix of both.

{kind=link}