The familiar weight of a leather wallet is becoming a vestigial organ of the global economy. Around the world, the tactile experience of paper bills and the metallic jingle of coins are being replaced by the silent haptics of a smartphone. As physical cash usage craters, we are witnessing more than just a shift in convenience; we are entering a era defined by the rise of Central Bank Digital Currencies (CBDCs). To the uninitiated, they sound like a technical update to a banking app, but for those of us watching the pulse of fintech, CBDCs represent the most fundamental re-engineering of money since the gold standard was abandoned. They are the state’s answer to a digital-first world, a strategic pivot to reclaim the financial narrative from private disruptors.

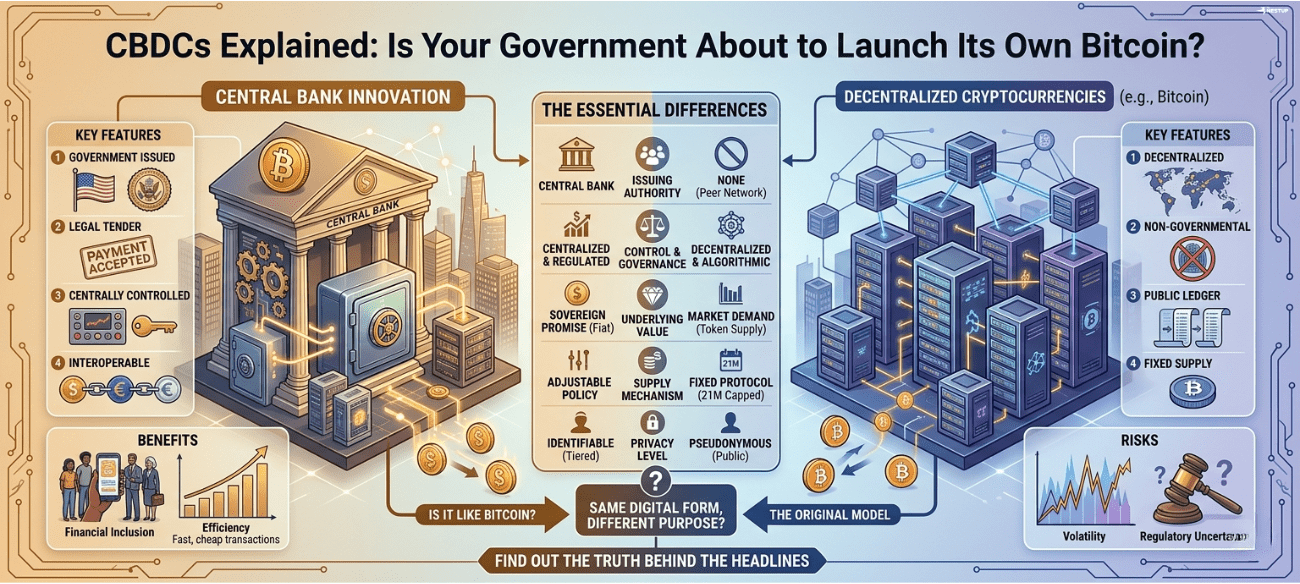

Takeaway 1: It’s Not “Government Bitcoin” (And That’s the Point)

The most common misconception is that a CBDC is simply a state-sponsored cryptocurrency. In reality, central banks are pivoting to defend their monetary monopoly, not to join a decentralized revolution. While Bitcoin is celebrated for being public, decentralized, and entirely outside of government reach, CBDCs are built on the exact opposite principles: they are centralized, permissioned, and designed to integrate seamlessly into existing state-controlled financial architectures. Governments aren’t looking to disrupt their own power; they are modernizing the tools of financial sovereignty to ensure that the issuance of money remains a state function in an era of private stablecoins and foreign payment networks.

“CBDCs are not trying to replace cryptocurrencies—they are governments adapting to a digital financial world… they are a digital extension of state-controlled money.”

Takeaway 2: Programmable Money is the Ultimate Economic Remote Control

China has already provided the world with a high-definition preview of this future. The digital yuan (e-CNY) isn’t just a pilot project; it is a massive deployment with millions of users already utilizing it for transportation, retail, and government services. What makes this revolutionary is “programmable money”—the ability for a central bank to code specific conditions directly into the currency itself.

This is the ultimate economic remote control. By removing the traditional banking middleman from the stimulus process, a government could implement monetary policy with surgical precision. Imagine stimulus payments that expire if not spent within 30 days to force immediate economic circulation, or interest rates applied directly to your digital wallet. This direct implementation bypasses the friction of commercial banks, giving policymakers unprecedented, real-time power over the velocity of money.

Takeaway 3: The Privacy Paradox—Digital Cash vs. State Surveillance

The shift toward CBDCs creates a fundamental tension between the streamlined efficiency of a digital ledger and the individual right to financial anonymity. Physical cash is the last bastion of untraceable economic behavior, but a digital currency controlled by a central bank offers the state a god-like view of every transaction within its borders. While supporters argue that CBDCs can be engineered with anonymized layers or strict limits on data collection to replicate the privacy of cash, the technical reality remains that a state-monitored ledger is inherently more visible than a paper bill.

This paradox is precisely why the European Union is moving with such calculated caution. European policymakers are currently locked in a debate over how to build a digital euro that safeguards civil liberties while remaining competitive. On the other side of the ledger, critics warn that without ironclad regulatory safeguards, CBDCs could morph into tools of total financial surveillance, giving governments the power to monitor—and potentially restrict—behavior based on spending patterns. It is this very lack of guaranteed privacy that is carving out a permanent market gap for private alternatives.

Takeaway 4: The U.S. “Infrastructure First” Stealth Strategy

While China moves at terminal velocity and the EU debates privacy frameworks, the United States is playing a sophisticated game of “infrastructure first.” The launch of FedNow is the centerpiece of this strategy. To be clear, FedNow is not a digital currency; it is the real-time payment plumbing that allows banks to settle transactions instantly. By focusing on the pipes rather than the water, the U.S. is modernizing its domestic system while carefully weighing the geopolitical risks of a digital dollar.

However, this “stealth” approach is not without risk. As the digital yuan gains utility in cross-border trade, the U.S. faces a growing challenge to its financial sovereignty and the dollar’s international dominance. The U.S. is moving slower because the stakes—financial stability, personal privacy, and the role of the state in private life—are higher for the world’s reserve currency. But make no mistake: by building the FedNow infrastructure, the U.S. is laying the technical foundation for a digital dollar to be activated the moment the political winds shift.

Takeaway 5: Stablecoins and CBDCs Will Likely Be “Frenemies”

There is a persistent narrative that the arrival of CBDCs will mean the death of private stablecoins. The reality will be far more nuanced: they are destined to be “frenemies.” While a state-backed digital dollar or euro might reduce the need for retail-focused stablecoins, private digital assets are expected to remain dominant in the world of Decentralized Finance (DeFi).

Stablecoins offer a level of interoperability and flexibility that centralized, permissioned CBDCs may never permit. Because a CBDC is an extension of state policy, it will likely be restricted by national boundaries and strict regulatory filters. Private stablecoins will continue to thrive by filling the gaps—serving as the lubricant for global, cross-platform transactions and providing the “permissionless” utility that state-controlled ledgers lack. We are headed toward a hybrid ecosystem where state and private digital assets coexist, each serving distinct corners of the global market.

Conclusion: The Balance of Power in a Digital Age

The momentum behind Central Bank Digital Currencies is now undeniable; several smaller economies have already crossed the finish line, and the world’s major powers are close behind. This is no longer a question of “if” our wallets will become fully digitized, but “when.” This transition marks a new chapter in the relationship between the citizen and the state, where the efficiency of the financial system is balanced against the autonomy of the individual.

As we stand on the threshold of this new financial era, we must confront a fundamental choice. Are we willing to trade the untraceable freedom of the paper dollar for the streamlined efficiency of a state-monitored ledger? The answer to that question will define the limits of financial freedom for the next century.

")

{kind=link}