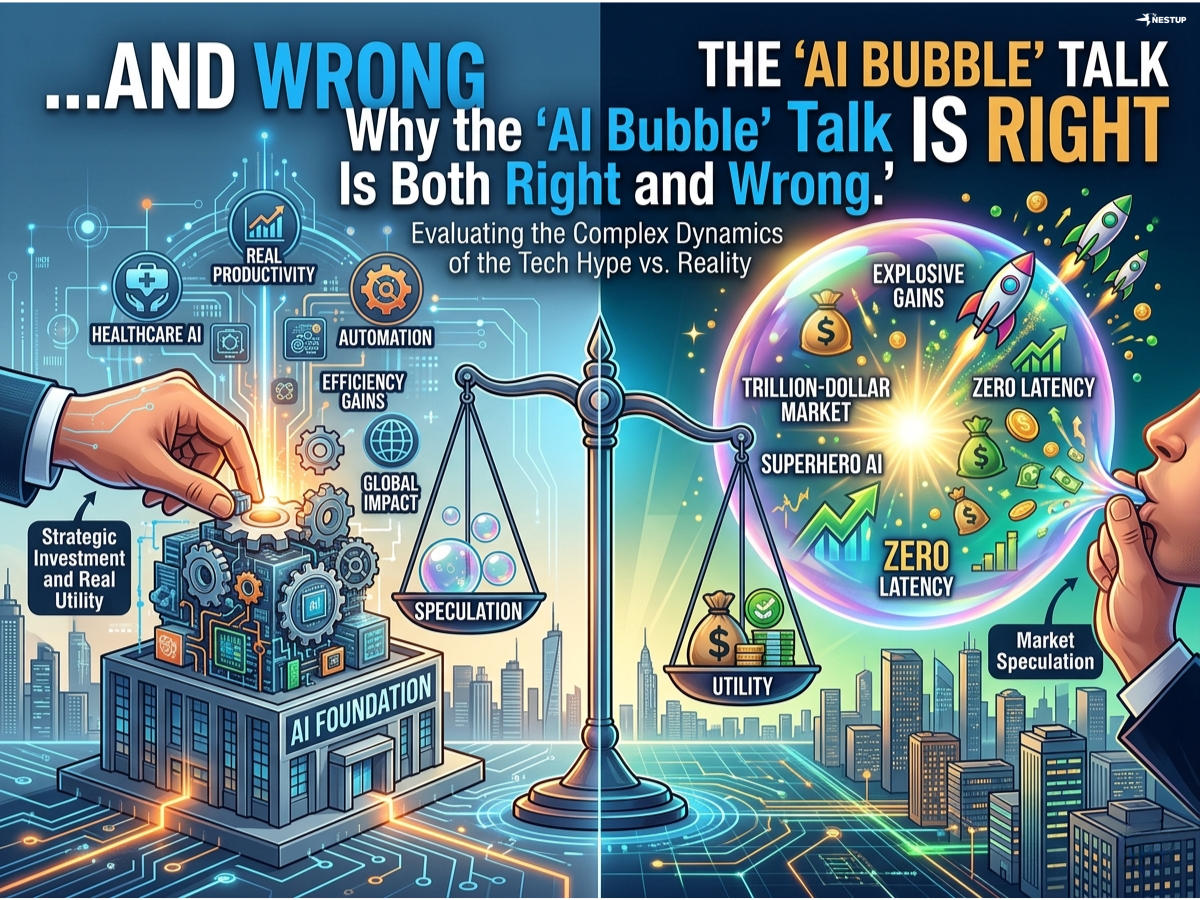

The Debate Isn’t Binary

The question “Are we in an AI bubble?” sounds simple—but the answer isn’t. In 2026, both sides of the argument are right, depending on where you look. Some parts of the AI market show clear signs of overheating, while others are generating real revenue and building long-term infrastructure.

This isn’t a classic bubble—or at least not a uniform one. It’s a layered market, where hype and fundamentals are coexisting in uncomfortable ways.

Why the Bubble Narrative Exists (And Has Real Evidence)

The strongest argument for an AI bubble comes from the sheer scale of spending. Big Tech is pouring hundreds of billions into AI infrastructure—data centers, GPUs, and model training—with expectations of future returns that are still uncertain. Recent reports show that major tech firms are collectively committing over $650 billion in AI-related capital expenditure in 2026 alone. (MarketWatch)

This level of investment has created a structural risk: overcapacity. If demand doesn’t grow fast enough to absorb all this compute, companies could be left with underutilized infrastructure—similar to what happened with fiber networks during the dot-com era.

There’s also the issue of revenue quality. A significant portion of AI revenue today comes from within the ecosystem itself—cloud providers selling compute to AI labs, which in turn build models used by other tech companies. Estimates suggest that only 30%–60% of AI revenue may come from true end customers, with the rest being intra-industry flows. (AI Magicx)

That circularity can inflate the perception of demand. It looks like growth—but part of it is companies effectively paying each other.

The Dot-Com Parallel: Familiar, but Incomplete

The comparison to the Dot-com bubble is not accidental. In both cases, a transformative technology triggered massive capital inflows, soaring valuations, and widespread speculation.

But the analogy only goes so far. During the dot-com era, many companies had little to no revenue. In contrast, today’s AI leaders are already generating billions. Companies like OpenAI, Microsoft, and Amazon are reporting significant AI-related revenue streams, in some cases reaching tens of billions annually. (The AI Tribune)

This is a crucial difference. The technology is not speculative—it is already being used, monetized, and embedded into real workflows.

The better comparison might be this: AI today looks less like 1999 internet hype and more like 2005–2010 cloud computing—real, growing, but still early in its economic impact.

The Revenue Is Real—But the Economics Are Messy

One of the most overlooked aspects of the AI boom is the gap between revenue and profitability. Yes, AI companies are making money. But many are also spending aggressively to sustain growth.

For example, some fast-growing AI startups have reached impressive revenue milestones while still operating with negative margins, meaning they lose money on each unit of usage. (The AI Tribune)

This creates a fragile dynamic. As long as growth continues, investors tolerate losses. But if growth slows or costs remain high—especially compute and energy costs—the economics could quickly come under pressure.

This is where the bubble argument gains strength. Not because AI lacks value, but because expectations may be ahead of reality.

Infrastructure Overbuild: The Biggest Hidden Risk

The most serious risk in the current cycle isn’t consumer adoption—it’s infrastructure overbuild. AI requires enormous amounts of compute, and companies are racing to secure capacity before competitors do.

This has led to extreme concentration. A handful of companies control the majority of AI infrastructure spending and supply chains. (AI Magicx)

If even one major player pulls back on spending, the effects could ripple across the entire ecosystem—from chipmakers to cloud providers to startups dependent on subsidized compute.

This kind of tightly coupled system is powerful during growth—but fragile during corrections.

Why the “No Bubble” Argument Also Holds Up

Despite these risks, dismissing the entire AI boom as a bubble misses a critical point: the underlying technology is delivering measurable value.

Studies show that AI is already improving productivity in real-world settings. In some cases, generative AI tools have increased worker productivity by 14% on average, and up to 35% for less-experienced workers. (The AI Tribune)

This matters because bubbles are usually driven by pure speculation. AI, by contrast, is already embedded in:

- Software development

- Customer support

- Marketing and content creation

- Enterprise automation

The demand is not hypothetical. It’s operational.

Where the Bubble Actually Is (Segment by Segment)

The reality is that the AI market is uneven. Some segments are clearly overheated, while others are relatively grounded.

Highly speculative areas include small-cap “AI-washed” companies and projects with little real revenue. These are the most likely to collapse in a correction.

More stable areas include large tech companies and infrastructure providers. While their valuations may be elevated, they are supported by real cash flow, diversified businesses, and long-term demand.

The strongest position may actually belong to “picks and shovels” players—chipmakers, data centers, and energy providers—because they benefit from the entire ecosystem regardless of which applications succeed.

What Survives a Correction (If It Happens)

If the market does correct, history provides a clear pattern. In the dot-com crash, most companies failed—but the infrastructure layer survived and eventually dominated.

The likely survivors in AI include:

- Companies with real revenue and paying customers

- Infrastructure providers supplying compute and networking

- Platforms with strong distribution and developer ecosystems

What tends not to survive are companies built purely on hype, without a clear path to profitability.

In other words, a correction would not kill AI—it would refocus it.

The Real Answer: It’s a Partial Bubble

The most accurate conclusion is that we are in a partial bubble. Some parts of the market are overheated and driven by speculation. Others are fundamentally strong and still early in their growth curve.

This dual reality is why the debate feels so polarized. Both sides are pointing at real evidence—they’re just looking at different parts of the system.

Final Takeaway: Hype Will Fade, Infrastructure Will Remain

The AI boom is not a mirage—but parts of it are inflated. The combination of massive capital spending, high valuations, and uncertain ROI creates conditions that resemble past bubbles.

At the same time, real revenue, real productivity gains, and real adoption suggest this is more than hype.

The most likely outcome is not a collapse, but a reset.

Expect volatility. Expect corrections. But also expect that the core of AI—the infrastructure, the use cases, and the companies with real economics—will emerge stronger on the other side.